It’s no accident that Spotify was launched in Sweden during the culmination of the The Pirate Bay lawsuit in 2008. Spotify was promoted as the legal alternative to P2P files haring and the Swedish music consumers were the perfect test market for such a Freemium music service. Sweden’s neighbouring country Norway was in a similar position: wealthy inhabitants, a high penetration of broadband Internet access and a passion for music. Therefore, the Swedish digital entertainment company Aspiro launched the music streaming provider WiMP (the later Tidal) in cooperation with the Norwegian telecommunication company Telenor and music retailer Platekompaniet in Norway in February 2010. Two months later WiMP also started in Denmark as the first music streaming service for PC, Mac and Android mobile.[1] However, in December 2009, the Danish telco TDC had added an unlimited streaming option to its music download service TDC Play (now YouSee Musik) in cooperation with tech company 24-7 Entertainment.[2] Thus, all three Scandinavian countries were pioneers in establishing a music streaming economy. The fourth Scandinavia country, Finland, lagged behind for some years, but in 2017 the Finnish sound recording market was as streaming-lined as its Scandinavian neighbours.

Figure 1: The global phonographic market in 2017 by digital market shares

Source: After IFPI Global Music Report 2018.

Source: After IFPI Global Music Report 2018.

A series of blog entries tells the story of how the Scandinavian countries have become the forerunners of the music streaming economy and highlights the background of this development. In this blog post a comparative analysis of market figures for all Scandinavian countries are presented.

Towards a music streaming economy – Scandinavia

Part 1: Market analysis

As highlighted in figure 1, Sweden, Norway, Finland and Denmark as well as Iceland had a streaming market share of the digital music market of more than 92 percent in 2017. In all five countries the download business is more or less irrelevant and the sales of physical products (CDs & vinyls) are very moderate. Thus, the Scandinavian recorded music market is a fully developed music streaming economy. The development, however, was not uniformly in the past few years.

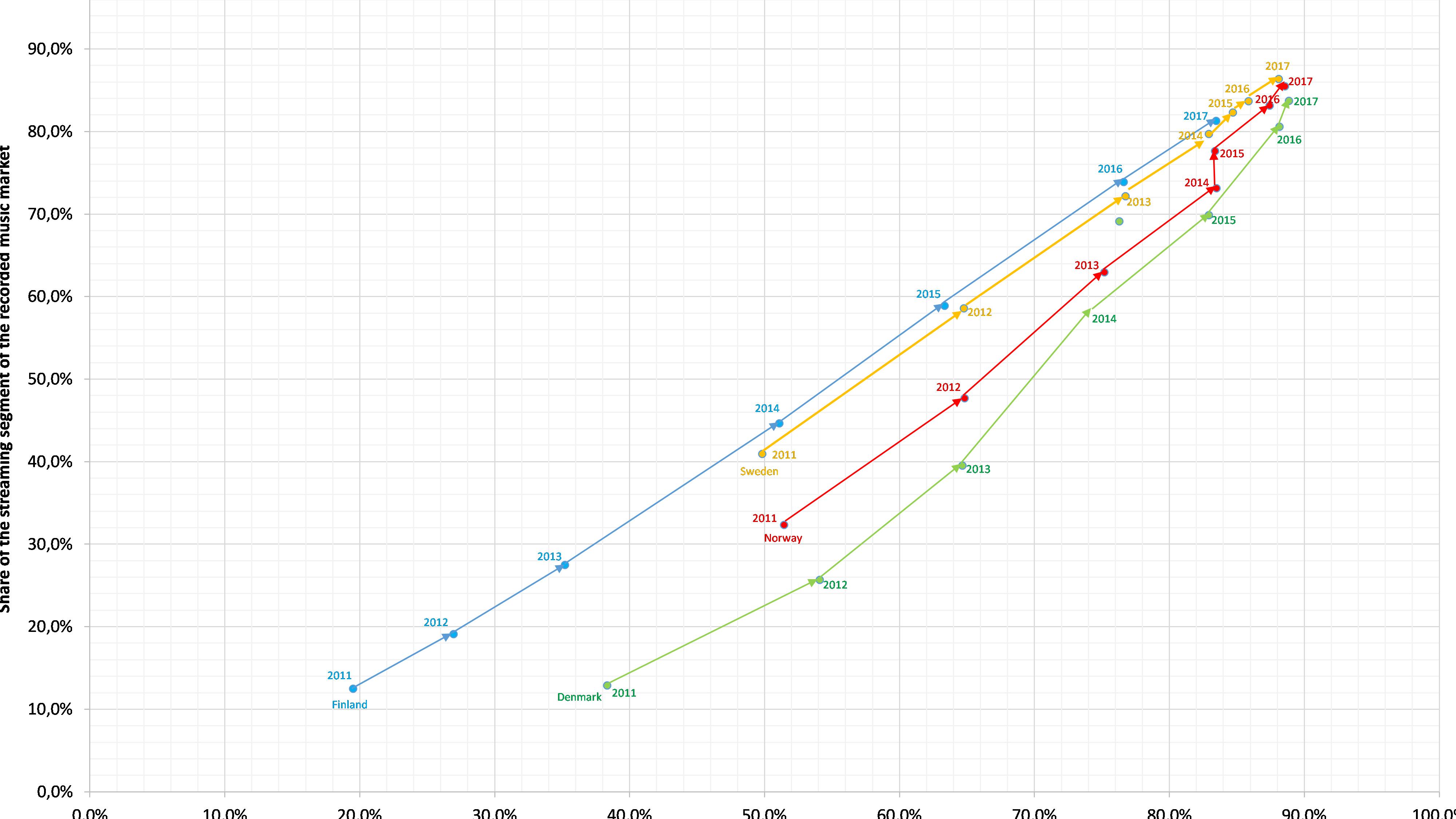

Figure 2: The way to the music streaming economy in Scandinavia, 2011-2017

Source: After IFPI Global Music Reports 2016 and 2018.

Source: After IFPI Global Music Reports 2016 and 2018.

Only Norway and Sweden had a well-developed digital music market with a market share of about 50 percent in 2011. At the same time Finland’s phonographic market was dominated by the physical product (mainly CDs) with a market share of more than 80 percent. In Denmark the CD sales were also still relevant with a share of more than 60 percent. In 2011, music streaming generated more than 40 percent of all digital music revenue in Sweden and Norway. In comparison, Finland and Denmark had an under-developed music streaming segment in 2011 with a digital music market share of about 12 percent. It took three more years to bring Finland to the same position as Sweden in 2011, since Finland had a strong physical market. In contrast, Denmark had become a digitized music economy in 2012 with digital music sales accounting for more that 50 percent of the overall recorded music revenue.

The digital market growth was driven by music streaming from 2011 to 2012: Denmark (+87.0), Finland (+55.3 percent), Norway (+59.1 percent) and Sweden (+73.6 percent). However, Denmark (+4.7 percent) and Finland (+16.2 percent) experienced also an increase of music download sales, whereas in Norway (-2.0 percent) and Sweden (-9.0 percent) the download market was already saturated.

Figure 3: The recorded music markets in Scandinavia, 2011-2017

Source: After IFPI Global Music Reports 2016 and 2018.

Source: After IFPI Global Music Reports 2016 and 2018.

After 2012, the download sales in all four Scandinavian countries decreased dramatically. From 2011 to 2017 the download market in Denmark lost 78.9 percent of its volume from US $17.11m to US $3.63m. In Norway the market decreased by 74.1 percent from US $13.06m to US $3.38m and in Sweden by 68.8 percent from US $8.26m to US 2.57m. Merely in Finland the loss of market volume was comparably lower with 35.6 percent from US $3.13m to US $1.09m. The decline of the download market was similar to the physical market in the same period: Denmark (‑76.9 percent from US $42.0m to US $9.7m), Finland (‑78.1 percent from US $38,8m to US $8.5m), Norway (‑62.5 percent from US $33.9m to US $12.7m) and Sweden (‑63.4 percent from US $53.3m to US $19.5m). Thus, the digital music market was only driven by the music streaming boom. The average annual growth rate of music streaming revenue from 2012 -17 ranges from 23.7 percent in Sweden to 45.9 percent in Denmark. The largest increase of music streaming revenue was in Denmark from US $8.79m to US $72.86m (+729 percent). In Finland music streaming revenue increased by 593 percent from US $6.03m to US $41.8m. Since the music streaming market in Norway and Sweden was already well developed in 2011, the increase was lower until 2017: Norway +320 percent from US $22.58m to US $94.72m and Sweden +225 percent from US $43.48m to US $141.34m.

In all four Scandinavian countries, however, music streaming over-compensated the loss of physical and download sales. The overall recorded music market in Sweden grew by 54.0 percent from 2011 to 2017. In Norway the growth rate was even higher with 58.7 percent. In Denmark recorded music sales increased by 27.8 percent and even in Finland the fast growing music streaming segment enabled a growth by 6.6 percent.

The growth of overall recorded music revenue in all Scandinavian countries indicates a convergence of all four markets to a music streaming economy. A closer analysis of the streaming segment highlights that the convergence process ended up in streaming markets with music subscription as the dominant revenue source. In Iceland all streaming revenue came from subscription music streaming, but also in Denmark, Norway and Sweden paid subscription accounted for more than 93 percent of the overall music streaming income. Only Finland lagged behind with an 87.6 percent share of subscription income in music streaming segment.

Figure 4: The music streaming markets in Scandinavia, 2016-2017

Source: After IFPI Global Music Report 2018.

Source: After IFPI Global Music Report 2018.

Figure 5: The music streaming markets in Scandinavia by revenue shares, 2016-2017

Source: After IFPI Global Music Report 2018.

Source: After IFPI Global Music Report 2018.

The Scandinavian music streaming markets follow different dynamics. In all countries the revenue from paid subscription increased from 2016 to 2017. However, the growth rates range from 3.7 percent in Norway to 19.3 percent in Finland. The revenue from ad-supported music streaming significantly differed in the five Scandinavian countries. In Iceland the ad-supported revenue went to zero in 2017 and in Sweden a decrease by 21.5 percent was reported. While ad-supported streaming income increased in Denmark, Finland and Norway – in Finland even by 23.6 percent. However, the most striking difference between Sweden on the hand and Denmark, Finland and Norway on the other is the revenue from music video streaming. In Sweden video streaming income decreased by 5.8 percent from 2016 to 2017, whereas in Norway the revenue from music video streams jumped from US $1.66m to US 4.08m (+145.8 percent). In Denmark and Finland the music video streaming income increased by 68.1 percent and 33.7 percent respectively.

Conclusion

All Scandinavian recorded music markets are dominated by music streaming yet. However, the path to a music streaming economy differs. While Swedes and Norwegians were early adopters of the music streaming services, the Danish and especially the Finns still bought CDs around 2010/11. Nevertheless Denmark and Finland made up the leeway by tremendous growth rates of the music streaming revenues in the following years. Despite a fully developed music streaming economy the four countries still differ in the adoption of paid subscription models and the use of music video streaming services. The following blog posts, therefore, analyse the different paths to a streaming economy in the Scandinavian countries and the rationale behind it.

Sources:

International Federation of the Phonographic Industry (IFPI), 2012, Recording Industry in Numbers. The Recorded Music Market 2011. London: IFPI.

International Federation of the Phonographic Industry (IFPI), 2015, Recording Industry in Numbers. The Recorded Music Market 2014. London: IFPI.

International Federation of the Phonographic Industry (IFPI), 2018, Global Music Report 2018. London: IFPI.

Endnotes

[1] Aspiro press release, “Aspiro and Telenor bring WiMP to Denmark”, April 10, 2010 (accessed: 29.03.2019).

[2] Music Ally, “TDC Play adds streaming music feature”, December 22, 2009 (accessed: 29.03.2019)

See also:

Towards a music streaming economy – Scandinavia part 2: technological and business model innovations

Towards a music streaming economy – Scandinavia part 3: consumer behavior

One thought on “Towards a music streaming economy – Scandinavia part 1”